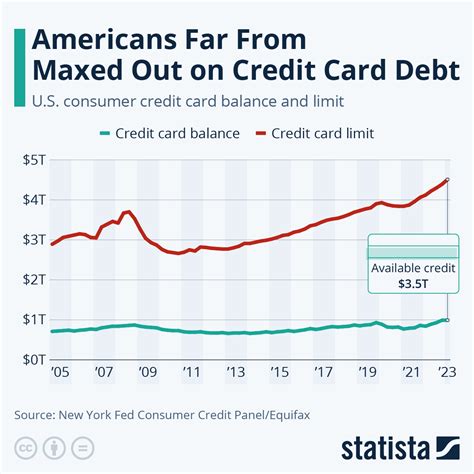

The issue of credit card debt and its implications during a government shutdown is a critical topic that affects millions of Americans. With the ever-looming threat of a potential shutdown, understanding the impact on personal finances, especially credit card debt, becomes increasingly important. This article aims to provide an in-depth analysis of how credit card debt can be affected by government shutdowns, offering valuable insights and practical advice to help individuals navigate this challenging situation.

Understanding the Impact of Government Shutdowns on Credit Card Debt

A government shutdown occurs when the federal government temporarily ceases operations due to a lack of funding, often resulting from a failure to pass a budget or a disagreement over policy issues. During a shutdown, non-essential federal employees are typically furloughed, and many government services are disrupted or halted.

When a government shutdown takes place, it can have far-reaching effects on the economy and, subsequently, on the personal finances of individuals. One of the most significant impacts is felt by those carrying credit card debt. The combination of lost income, reduced access to credit, and potential changes in interest rates can create a perfect storm for those already struggling with debt.

Lost Income and Delayed Payments

For federal employees affected by a shutdown, the immediate concern is often the loss of income. While some employees may be considered essential and continue to work without pay, others are placed on furlough, meaning they are not allowed to work and do not receive any compensation. This loss of income can be devastating for those who rely on their salaries to cover basic living expenses, including credit card payments.

Even for those who are not directly employed by the federal government, a shutdown can still impact their financial situation. Businesses that depend on government contracts or grants may experience delays or cancellations, leading to reduced revenue and potential job losses. These ripple effects can further strain the ability of individuals to make timely credit card payments.

| Impact on Federal Employees | Consequences |

|---|---|

| Lost Income | Difficulty making credit card payments |

| Furlough | Increased risk of default or late payments |

| Delayed Reimbursements | Accumulation of debt |

Reduced Access to Credit and Increased Interest Rates

During a government shutdown, lenders may become more cautious about extending credit. This is due to the uncertainty surrounding the economy and the potential for widespread financial distress. As a result, individuals may find it more challenging to obtain new credit cards or loans, limiting their options for managing their existing debt.

Furthermore, credit card companies may adjust their interest rates during a shutdown. While some lenders may offer temporary relief by waiving late fees or reducing interest rates for affected customers, others may take the opposite approach. In a volatile economic environment, lenders may increase interest rates to mitigate their risk, making it more expensive for cardholders to carry a balance.

Strategies for Managing Credit Card Debt During a Shutdown

While a government shutdown can present significant challenges, there are strategies that individuals can employ to navigate their credit card debt more effectively during this difficult time.

Prioritize Payments and Seek Assistance

During a shutdown, it’s crucial to prioritize your credit card payments. Focus on making at least the minimum payments to avoid late fees and negative impacts on your credit score. If you’re facing financial hardship, reach out to your creditors and explain your situation. Many lenders offer hardship programs or temporary relief options, such as payment deferrals or reduced interest rates, to help customers during difficult times.

Additionally, consider seeking assistance from government or nonprofit organizations that offer financial counseling and debt management services. These organizations can provide guidance on budgeting, debt repayment plans, and negotiating with creditors. They may also have resources to help you access emergency funds or alternative sources of income during the shutdown.

Explore Debt Consolidation Options

Debt consolidation can be a viable strategy to simplify and manage your credit card debt more effectively. By consolidating your debts into a single loan or balance transfer credit card, you may be able to reduce your interest rates and simplify your monthly payments. This can be especially beneficial during a government shutdown when managing multiple credit card payments may become more challenging.

However, it's important to carefully evaluate the terms and conditions of any debt consolidation option. Ensure that the interest rate and fees are reasonable and that you can afford the new payment terms. Consider consulting with a financial advisor or credit counselor to determine the best consolidation option for your situation.

Build an Emergency Fund and Improve Financial Resilience

One of the best ways to prepare for unexpected financial challenges, such as a government shutdown, is to build an emergency fund. Aim to save at least three to six months’ worth of living expenses to provide a financial cushion during periods of reduced income. This fund can help cover essential expenses and reduce the need to rely on credit cards during difficult times.

Additionally, focus on improving your financial resilience by adopting healthy money habits. Create a realistic budget, track your spending, and look for ways to cut costs. Consider negotiating lower interest rates with your credit card companies or exploring opportunities to increase your income through side hustles or part-time work. By taking proactive steps to manage your finances, you can better weather the storms of government shutdowns and other financial crises.

The Long-Term Impact and Policy Considerations

While this article has focused primarily on the immediate effects of a government shutdown on credit card debt, it’s important to consider the long-term implications as well. Repeated shutdowns or prolonged periods of economic uncertainty can have lasting effects on an individual’s financial health and the broader economy.

Policy makers and lawmakers have a crucial role to play in preventing or minimizing the impact of government shutdowns. By working together to find bipartisan solutions and ensuring timely budget approvals, they can help avoid the financial hardships experienced by millions of Americans. Additionally, policymakers should consider implementing measures to protect consumers during periods of economic distress, such as providing emergency financial assistance or strengthening consumer protection laws.

Advocating for Financial Education and Consumer Protection

Beyond the immediate crisis, there is a need for ongoing financial education and consumer protection efforts. Empowering individuals with the knowledge and tools to manage their finances effectively can help them navigate not only government shutdowns but also a wide range of financial challenges. Financial literacy programs, accessible credit counseling services, and transparent lending practices can all contribute to a more resilient and financially secure population.

Conclusion

Government shutdowns present unique challenges for individuals managing credit card debt. By understanding the potential impacts and implementing strategic financial management techniques, individuals can navigate these difficult times more effectively. It is essential for policymakers, financial institutions, and consumers to work together to address the underlying causes of shutdowns and to create a more stable and supportive financial environment for all.

What happens to credit card interest rates during a government shutdown?

+Credit card interest rates can vary during a government shutdown. Some lenders may offer temporary relief by reducing interest rates for affected customers, while others may increase rates to mitigate risk. It’s important to review your credit card terms and contact your lender to understand any changes.

Are there government programs to assist with credit card debt during a shutdown?

+While there are no specific government programs solely dedicated to assisting with credit card debt during a shutdown, federal employees may be eligible for certain benefits or financial relief through their agency or union. It’s advisable to check with your employer or union representative for more information.

How can I protect my credit score during a government shutdown?

+To protect your credit score during a government shutdown, prioritize making at least the minimum payments on your credit cards. Late or missed payments can negatively impact your credit score. If you’re facing financial hardship, reach out to your creditors to explore hardship programs or payment relief options.